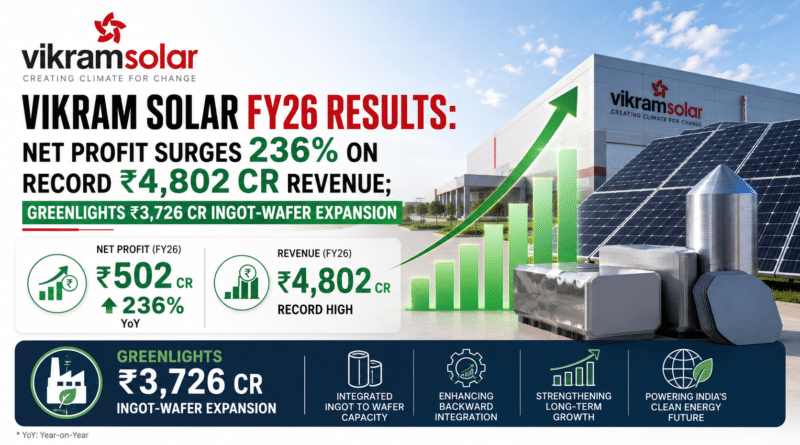

Vikram Solar Q4 and FY26 Results Conference Call: ₹4,802 Cr Revenue

Vikram Solar’s Q4 and FY 2026 earnings conference call, held on May 8, 2026, highlighted a landmark year of record-breaking

Read More

Vikram Solar’s Q4 and FY 2026 earnings conference call, held on May 8, 2026, highlighted a landmark year of record-breaking

Read More

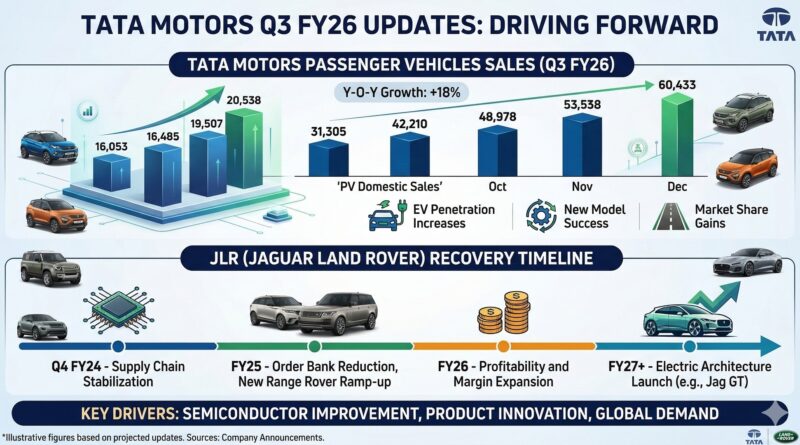

Tata Motors Q3 FY26 Concall: Understanding JLR Problems and What Investors Should Expect Next The Q3 FY26 earnings call of

Read More

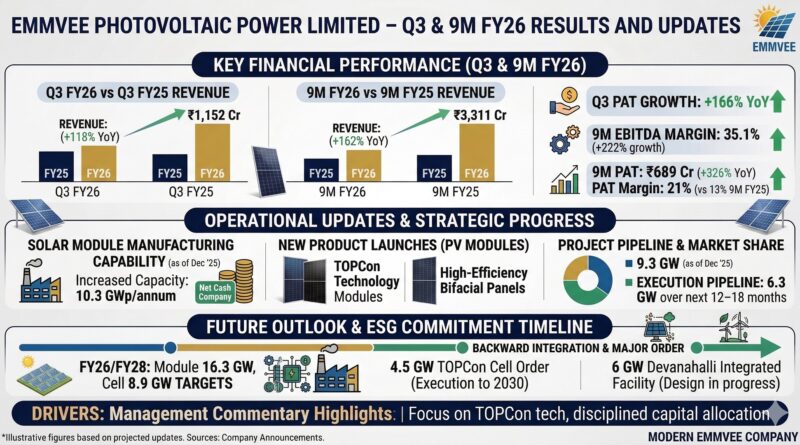

Emmvee Photovoltaic Power Limited – Q3 & 9M FY26 Results Emmvee Photovoltaic Power Limited has delivered an exceptionally strong performance

Read More

Ola Electric and TVS Motor: A Tale of Two Eras of Growing Pains and Maturity If you’ve been tracking India’s

Read More

Tesla Q3 2024 Conference Call Summary and Future Outlook Tesla, the electric vehicle (EV) leader, recently held its Q3 2024

Read More

Quarterly Performance Highlights of Raymond Lifestyle Raymond Lifestyle Limited demonstrated resilience in Q2 FY25 despite challenging macroeconomic conditions. The company

Read More

Investing is a powerful way that can help you build wealth, secure your financial future, and achieve your long-term goals.

Read More

EaseMyTrip.com Q4 (2023-24) Con Call Summary On May 24, 2024, Easy Trip Planners Limited held its Q4 FY2024 earnings call,

Read More

If you’re planning to bring your parents or grandparents to Canada for an extended stay, you’ve likely heard about the

Read More